“Britain’s world-leading music sector has the potential for sustained growth in the years ahead, but this exciting future can only be realised if government makes creative businesses a priority post-Brexit.”

London, 13th April 2017 – UK record company trade income1 – the combined revenues generated through streaming, sales of music across physical and download formats, performance rights, and ‘sync’ music licenced for use in film & TV, games and advertising – rose by just over five per cent (5.1%) in 2016, reports labels’ association the BPI. Trade income of ?926 million represents the largest annual total in five years.

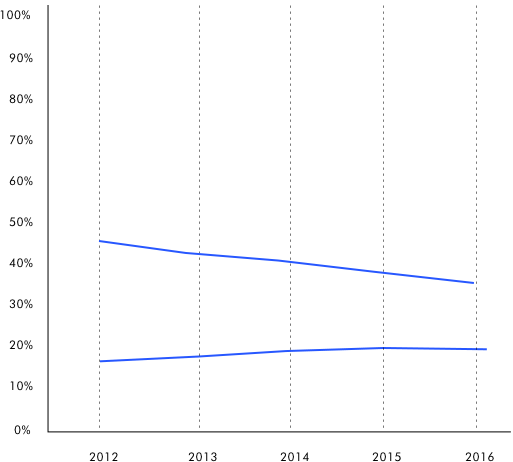

The ?44.6 million trade income rise on 2015 was driven largely by the dynamic growth in streaming revenues – a 61 per cent increase which more than offset the decline in income from physical formats and downloads. It also meant that streaming accounted for 30 per cent of overall label revenues in 2016 (compared to physical at 32 per cent). Such a rate of growth will undoubtedly see the format overtake physical to become the leading contributor to label revenues in 2017.

Revenue growth was largely experienced in Q2 and Q3, whilst Q4, traditionally the industry’s biggest sales period, grew by only 0.4 per cent, although that compares to Q4 2015 which included the release of Adele’s album 25.

Whilst the increase in revenues is to be welcomed, there remain a number of structural challenges that inhibit growth, including illegal websites and the “Value Gap”. The latter term describes the growing mismatch between the huge value that certain digital platforms, such as YouTube, extract from music or other entertainment and the relatively small amount they return back to the creators concerned.

The UK recorded music industry also faces stronger competition on global streaming platforms and will need to work with government to ensure that, post-Brexit, UK artists retain access to EU markets, and that weak IP regimes are strengthened in key export markets.

Market share breakdown by revenue stream 2012 – 2016

Market share breakdown by revenue stream 2012 – 2016

Subscriptions fuel streaming growth

Subscription forms the key element of streaming revenues, accounting for 87.1 per cent of the annual market total of ?274 million. Income from ad-supported tiers of audio streaming services represents just 3.6 per cent, and video streaming 9.3 per cent.

Consumer uptake of premium subscription services such as Spotify, Apple Music and Deezer continues to rise. For the four-weeks ending 18th December 2016, Kantar research reported that 11 per cent of the UK adult population used a paid-for service, up from 9 per cent from the same period in 2015. This suggests the continued offer of free trials, above-the-line advertising and bundled deals are helping to drive engagement

“UK record labels will continue to take huge risks backing emerging British talent and investing hundreds of millions of pounds annually to bring it to a global audience. With strong support from government, British music can continue to be a global success.”

Physical formats remain resilient, with vinyl now accounting for nearly 5 per cent of revenues

Subscription forms the key element of streaming revenues, accounting for 87.1 per cent of the annual market total of ?274 million. Income from ad-supported tiers of audio streaming services represents just 3.6 per cent, and video streaming 9.3 per cent.

Consumer uptake of premium subscription services such as Spotify, Apple Music and Deezer continues to rise. For the four-weeks ending 18th December 2016, Kantar research reported that 11 per cent of the UK adult population used a paid-for service, up from 9 per cent from the same period in 2015. This suggests the continued offer of free trials, above-the-line advertising and bundled deals are helping to drive engagement

Performance rights and ‘sync’ earnings also on the up

Record company earnings from performance rights collected by PPL2 from the broadcast and public performance of recorded music3 increased by 1.8 per cent in 2016 from ?171 million in 2015 to ?174 million. Over the same period, revenues generated from the licensing of ‘sync’ music3 for use in film & TV, games and advertising also rose, though by a more modest 0.6 per cent.